Debt Snowball Method and Debt Avalanche Method are the two most popular strategies to get out of debt in 2026. If you are carrying credit card balances, personal loans, or medical bills, choosing the right debt payoff method can mean the difference between becoming debt-free in 2 years — or still struggling 5 years from now.

In this complete guide, we compare both methods side by side with real numbers, explain exactly how each one works, and help you decide which proven strategy fits your situation best. Ready to run the numbers on your own debts? Try our free Debt Payoff Planner at ClearMyDebtUSA.com.

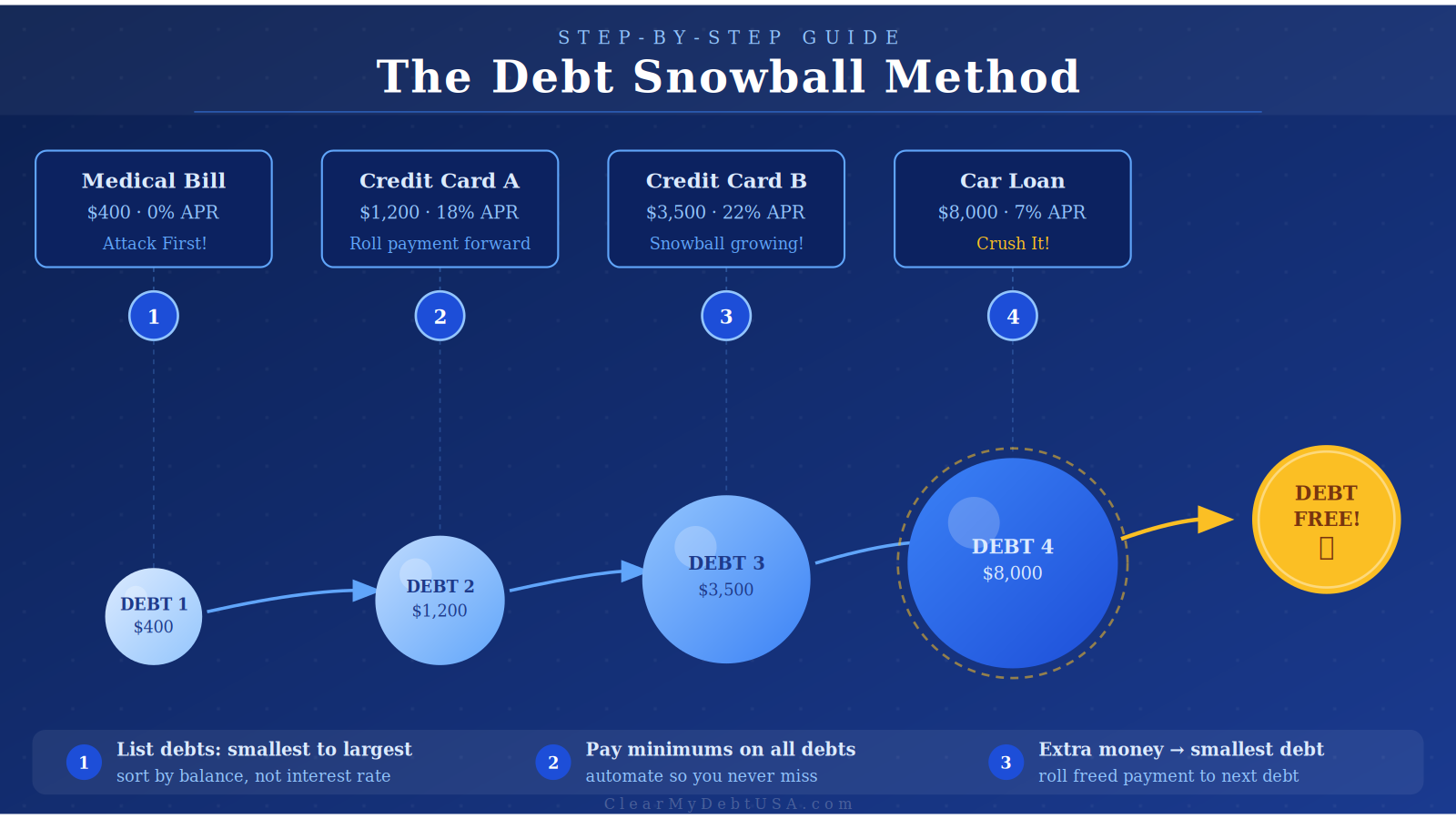

What Is the Debt Snowball Method?

The Debt Snowball Method was made famous by personal finance expert Dave Ramsey. The core idea is powerful in its simplicity: pay off your smallest debt first, no matter the interest rate. As each small debt disappears, you roll that freed-up payment into the next one — like a snowball gaining size and speed rolling downhill.

How the Debt Snowball Method Works — Step by Step

- List all your debts from smallest balance to largest.

- Make minimum payments on every debt each month.

- Direct every extra dollar toward the smallest balance.

- Once that debt hits zero, add that payment amount to the next smallest debt.

- Repeat until you are completely debt-free.

Debt Snowball Method: Real Example

Say you have these four debts:

- Medical bill: $400 at 0% interest

- Credit Card A: $1,200 at 18% APR

- Credit Card B: $3,500 at 22% APR

- Car loan: $8,000 at 7% APR

With the Debt Snowball Method, you attack the $400 medical bill first — even though it carries zero interest. Knock it out, then stack that payment on top of Credit Card A’s minimum, then Credit Card B, then the car loan.

According to research from the Harvard Business School, people who focus on paying off one account at a time are significantly more likely to eliminate all their debt — proving the psychology behind the Debt Snowball Method is just as important as the math.

What Is the Debt Avalanche Method? (Debt Snowball Method Alternative)

The Debt Avalanche Method is the mathematically optimal way to pay off debt. Instead of the smallest balance, you target the highest interest rate debt first. This approach minimizes the total interest you pay and — if followed perfectly — gets you debt-free slightly faster than the Debt Snowball Method.

How the Debt Avalanche Method Works — Step by Step

- List all your debts from highest interest rate to lowest.

- Make minimum payments on every debt each month.

- Put every extra dollar toward the highest-APR debt.

- Once that debt is paid off, move to the next highest interest rate.

- Repeat until debt-free.

Debt Avalanche Method: Real Example

Using the same debts:

- Credit Card B: $3,500 at 22% APR ← Attack this first

- Credit Card A: $1,200 at 18% APR

- Medical bill: $400 at 0% interest

- Car loan: $8,000 at 7% APR

You go after Credit Card B first because that 22% interest is the most expensive debt you carry. By eliminating the highest-rate debt first, you stop the most costly interest from compounding. As the Federal Trade Commission (FTC) advises, tackling high-interest debt aggressively is one of the most effective debt reduction strategies available.

Debt Snowball Method vs Debt Avalanche: Side-by-Side Comparison

| Factor | Debt Snowball Method ❄️ | Debt Avalanche Method 🏔️ |

|---|---|---|

| Debt priority order | Smallest balance first | Highest interest rate first |

| Total interest paid | Slightly higher | Lower — saves more money |

| Time to first win | Faster quick wins | Slower initial progress |

| Motivation level | ⭐⭐⭐⭐⭐ Very high | ⭐⭐⭐ Moderate |

| Best for | People who need momentum | Disciplined, numbers-focused people |

| Difficulty to follow | Easy | Requires strong discipline |

| Math vs Psychology | Psychology-first approach | Math-first approach |

Real Numbers: Does the Debt Snowball Method Pay Off Debt Faster?

Here is a realistic scenario. You have $500/month extra to put toward debt:

- Credit Card A: $800 at 15% APR

- Credit Card B: $2,400 at 20% APR

- Personal Loan: $5,000 at 11% APR

- Car Loan: $9,000 at 6% APR

❄️ Debt Snowball Method

✅ Debt-free in ~38 months

💸 Total interest: ~$3,200

🏆 First win: Month 2

🏔️ Debt Avalanche Method

✅ Debt-free in ~36 months

💸 Total interest: ~$2,750

🏆 First win: Month 6

The Avalanche saves roughly $450 and 2 months. But the Debt Snowball Method gives you your first zero-balance account in just 2 months versus 6 months with the Avalanche. For most people, that psychological win is worth far more than $450. According to Experian’s debt payoff research, staying motivated is the single biggest factor in successfully eliminating debt.

Want to calculate your exact payoff date? Use our free Debt Payoff Planner at ClearMyDebtUSA.com.

When to Choose the Debt Snowball Method

The Debt Snowball Method is the right choice if:

- You have struggled to stick to debt plans before and need early motivation.

- Your interest rates are similar across most debts (the math difference is small).

- You have several small debts cluttering your finances.

- You feel overwhelmed and need an emotional win quickly.

- You are new to structured debt payoff and want a simple system to follow.

The Debt Snowball Method works because it leverages human psychology. Every time a debt hits zero, your brain gets a motivational boost — reinforcing the habit of paying off debt and keeping you on track to continue.

When to Choose the Debt Avalanche Method

Choose the Debt Avalanche Method if:

- You are highly disciplined and stay motivated by tracking numbers — not wins.

- You have one or two debts with very high interest rates (20%+).

- Saving the maximum amount of money is your primary goal.

- Your highest-interest debt also happens to be a smaller balance (fast win + interest savings).

- You have a long-term mindset and are not driven by immediate gratification.

Can You Combine the Debt Snowball Method and Avalanche Method?

Yes — and a hybrid approach works exceptionally well for many people:

- Start with the Debt Snowball Method to eliminate 1–2 small debts and build confidence.

- Once you feel motivated, switch to the Avalanche Method to minimize interest on your remaining larger debts.

This is especially powerful when you have a mix of small low-interest debts (like medical bills) and large high-interest debts (credit cards). Use the Snowball Method to clear the clutter, then use the Avalanche to destroy the expensive stuff.

5 Proven Tips to Make the Debt Snowball Method Work Faster

Whichever method you choose, these 5 steps will speed up your progress significantly:

- Find extra money every month. Even $50–$100 extra per month accelerates payoff dramatically. See: 9 Proven Ways to Find Extra Money for Debt Payoff.

- Negotiate your interest rates down. A simple phone call can lower your APR. Here is exactly how: How to Lower Your Credit Card Interest Rate.

- Stop adding new debt immediately. Put your credit cards in a drawer. Every new charge resets your Debt Snowball Method progress.

- Automate your payments. Set minimum payments on autopay so you never miss a due date and never skip a month.

- Track your progress visually. Seeing balances drop is incredibly motivating. Use our free planner at ClearMyDebtUSA.com to watch your debt-free date get closer every month.

Debt Snowball Method vs Debt Avalanche: The Honest Verdict

Both the Debt Snowball Method and the Debt Avalanche Method are proven, battle-tested strategies for becoming debt-free. Here is the ultimate decision guide:

👉 Need motivation and fast wins? → Use the Debt Snowball Method.

👉 Disciplined and want to save the most money? → Use the Debt Avalanche Method.

👉 Not sure which fits you? → Start with the Debt Snowball Method. You can always switch once you have momentum.

The most important decision you can make right now is to start today. Every month you delay costs you more in interest charges and pushes your debt-free date further away.

Make a real plan in under 2 minutes — use our free Debt Payoff Planner at ClearMyDebtUSA.com. Enter your balances, choose the Debt Snowball Method or Avalanche, and see your exact debt-free date instantly.

Frequently Asked Questions About the Debt Snowball Method

Is the Debt Snowball Method or Debt Avalanche better?

The Debt Snowball Method is better for people who need motivation and early wins. The Debt Avalanche is better for disciplined people who want to minimize total interest paid. Research consistently shows that the best method is whichever one you will actually stick to.

How much faster is the Debt Avalanche vs Debt Snowball Method?

On average, the Debt Avalanche is 1–3 months faster and saves between a few hundred and a few thousand dollars in interest — depending on your specific balances and interest rates.

Does the Debt Snowball Method actually work?

Yes. The Debt Snowball Method has helped millions of Americans become debt-free. Its effectiveness is backed by behavioral economics research showing that small wins create the motivation needed to sustain long-term financial discipline.

Can I switch from the Debt Snowball Method to the Avalanche?

Absolutely. Many people start with the Debt Snowball Method to build confidence, then switch to the Avalanche method once they have momentum and feel in control of their finances.

What if I only have one debt?

If you have just one debt, the Debt Snowball Method and Debt Avalanche Method are identical. Simply put every extra dollar you can toward that one balance as aggressively as possible.

What is the average amount of debt Americans carry?

According to Experian’s 2025 Consumer Debt Study, the average American carries $104,755 in total debt, with credit card balances averaging $6,735 per person — making strategies like the Debt Snowball Method more important than ever.

For more free debt payoff tools, step-by-step guides, and calculators, visit ClearMyDebtUSA.com — your free resource for becoming debt-free in 2026.