📋 In This Article

If you’re carrying multiple debts — credit cards, personal loans, medical bills — and tired of watching your balances barely move, the debt avalanche method is the most mathematically efficient way to get out of debt. Period.

But knowing the method isn’t enough. You need an actual debt avalanche calculator that shows you exactly which debt to attack first, how much to pay each month, and when you’ll finally be free.

That’s exactly what our free planner tool does. No email required. No signup. Just results.

🎯 Try the Free Debt Avalanche Calculator

Enter your debts, choose avalanche, get your exact payoff date + PDF plan

What Is a Debt Avalanche Calculator?

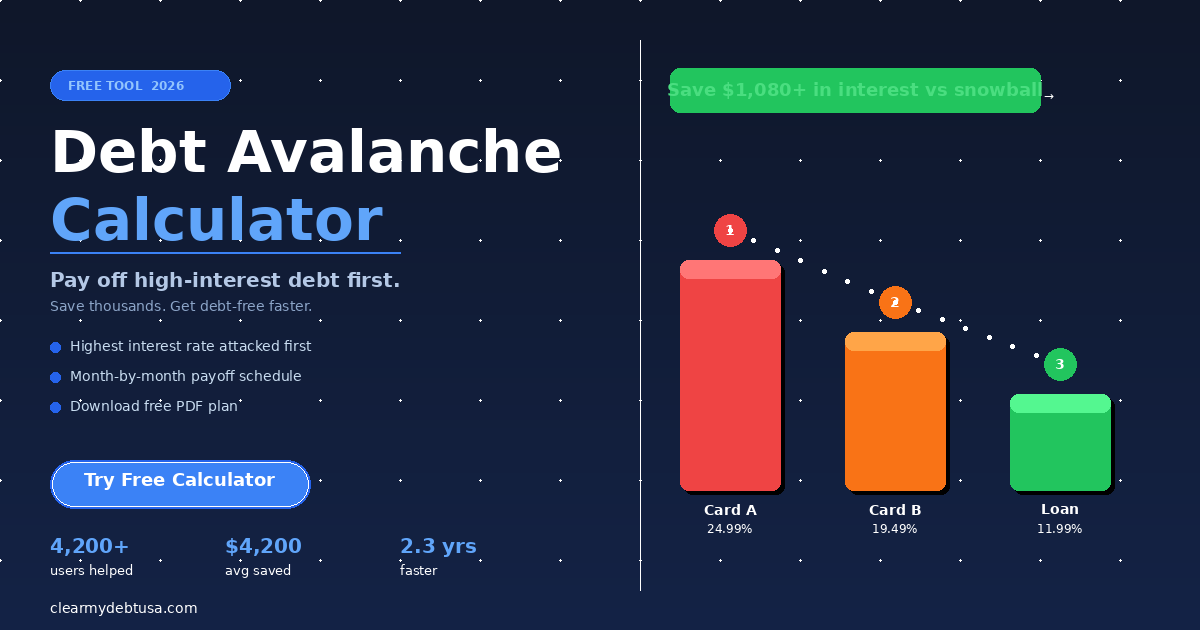

A debt avalanche calculator is a free tool that applies the avalanche repayment strategy to your specific debts. You enter each debt’s balance, interest rate, and minimum payment. The calculator then:

- Ranks your debts from highest to lowest interest rate

- Calculates exactly how to allocate your extra monthly payment

- Shows you a month-by-month payoff schedule

- Tells you the exact date you’ll become debt-free

- Shows how much interest you’ll save compared to minimum payments only

Without a calculator, it’s nearly impossible to figure this out manually — especially if you have 3, 4, or 5 different debts with different rates and balances. The math compounds every single month.

How the Debt Avalanche Method Works

The debt avalanche method follows one simple rule: always attack the highest-interest-rate debt first, while making minimum payments on everything else.

Once that debt is paid off, you “roll” its entire payment into the next highest-rate debt. This rolling effect creates an accelerating payoff — each debt falls faster than the last.

A Simple Example

Say you have these 3 debts and $600/month to put toward them:

| Debt | Balance | APR | Min Payment |

|---|---|---|---|

| Chase Credit Card | $4,500 | 24.99% | $112 |

| Capital One Card | $2,800 | 18.99% | $70 |

| Personal Loan | $7,200 | 12.50% | $180 |

With the avalanche method:

- Pay $112 + $70 + $180 = $362 in minimums

- Take remaining $238 and dump it on Chase (highest APR at 24.99%)

- Once Chase is paid off, roll its $350 payment into Capital One

- Once Capital One is gone, everything attacks the personal loan

The result? You pay off all three debts significantly faster and save hundreds — sometimes thousands — in interest compared to paying minimums only.

💡 Key Insight: The avalanche method saves the most money mathematically. It works because high-interest debt grows faster than low-interest debt. Every dollar you delay paying on a 25% card costs you more than every dollar delayed on a 12% loan.

How to Use Our Free Debt Avalanche Calculator

Our free planner at ClearMyDebtUSA takes under 3 minutes to set up. Here’s exactly what to do:

Step 1: Gather Your Debt Information

Before you open the calculator, find these 3 numbers for each debt:

- Current balance — check your latest statement

- APR (Annual Percentage Rate) — also on your statement, usually in the “interest charges” section

- Minimum monthly payment — the minimum due, not what you’re currently paying

Step 2: Enter Your Debts

Add each debt — credit cards, medical bills, personal loans, student loans — into the planner. You can add up to as many debts as you need.

Step 3: Select “Avalanche” Strategy

Choose the Avalanche method. The calculator automatically ranks your debts by highest interest rate first and builds your payoff plan.

Step 4: Add Extra Monthly Payment (Optional)

If you can pay even $50–$100 extra per month, enter it here. You’ll be shocked how much faster your payoff date moves.

Step 5: Download Your PDF Plan

Get a complete month-by-month schedule showing exactly what to pay, when, and how your balances shrink. No email required.

Use the Free Calculator Now

Compare avalanche vs snowball side by side for your exact situation

Debt Avalanche vs Debt Snowball: Real Numbers

The other popular debt payoff strategy is the snowball method — pay off the smallest balance first for psychological wins. Both work. But which one saves more money?

Let’s use a real $18,500 debt scenario with $700/month total payment budget:

| Debt | Balance | APR |

|---|---|---|

| Credit Card A | $3,200 | 22.99% |

| Credit Card B | $5,800 | 19.49% |

| Personal Loan | $9,500 | 11.99% |

| 🎯 Avalanche | ❄️ Snowball | |

|---|---|---|

| Total Interest Paid | $3,840 | $4,920 |

| Months to Pay Off | 31 months | 32 months |

| Interest Savings | $1,080 saved | — |

In this scenario, avalanche saves $1,080 in interest and pays off 1 month faster. The difference grows larger when your high-interest debt has a bigger balance.

When is snowball better? If you have 5+ small debts and need the motivational boost of clearing debts quickly — snowball keeps more people on track. A plan you stick to beats a plan you abandon.

Our calculator lets you compare both side by side instantly with your own numbers.

When Should You Use the Avalanche Method?

The avalanche method is the right choice when:

- You have high-interest credit card debt — anything above 18% APR is costing you serious money every single month

- You’re disciplined and numbers-motivated — you can stay focused even when your first payoff target takes several months

- Your highest-rate debt is also reasonably sized — if your 25% APR card has a $15,000 balance, you’ll be paying on it for a long time before that first win

- Saving the maximum amount of money is your top priority

The avalanche method is NOT ideal when:

- Your highest-interest debt is also your largest — you’ll wait months before seeing any debt disappear

- You’ve struggled to stay motivated with debt payoff in the past

- You have many small debts that are mentally cluttering your finances

⚡ Pro Tip: Use our calculator to compare both methods for YOUR specific debts. The “right” answer depends entirely on your numbers — there’s no universal winner without running your actual situation.

3 Mistakes People Make with the Avalanche Method

Mistake 1: Not Including All Debts

Most people forget to include medical bills, store cards, or old personal loans. Every debt that’s charging you interest needs to be in your calculator. Missing one debt means your payoff plan is wrong from day one.

Mistake 2: Not Adding Extra Payments

The avalanche method works on minimum payments alone — but it works dramatically faster with even small extra contributions. An extra $100/month on a $10,000 balance at 20% APR saves over $2,800 in interest and cuts nearly 18 months off your timeline. Even $50 makes a real difference.

Mistake 3: Switching Methods Halfway Through

Some people start avalanche, get impatient when their first payoff target takes a while, and switch to snowball mid-plan. This is the worst move. You’ve already paid the “patience cost” of attacking the high-interest debt. Switching now means you gave up the savings without getting the reward. Stick to whichever method you start with.

Frequently Asked Questions

Is the debt avalanche method the best way to pay off debt?

Mathematically, yes — the avalanche method saves the most money in interest of any debt payoff strategy. Whether it’s the “best” for you personally depends on how you stay motivated. If you need quick wins to stay on track, the snowball method may actually get you out of debt faster because you won’t quit.

How much money does the debt avalanche method save?

It depends on your specific debts. The bigger the gap between your highest and lowest interest rates, the more you save. On a typical $15,000–$25,000 debt portfolio, most people save between $800 and $3,500 compared to the snowball method — and save thousands more compared to minimum payments only.

How long does the debt avalanche method take?

This depends entirely on your total debt amount, interest rates, and how much extra you pay each month. Use our free calculator above to get your exact payoff timeline — it calculates to the month.

Can I use a debt avalanche calculator for student loans?

Yes. The avalanche method works for any type of debt — credit cards, student loans, personal loans, medical bills, auto loans. Just make sure to enter the correct APR for each loan. Federal student loans may have special repayment or forgiveness options you should consider separately.

What if I can’t afford more than minimum payments?

Even minimum payments following the avalanche order — paying any extra, even $20, toward the highest-rate debt — will save you money. If you’re genuinely struggling, our planner includes a $3 consultation option where a debt advisor can walk you through hardship programs, rate negotiation, and consolidation options that might lower your payments significantly.

Does the debt avalanche method hurt your credit score?

No. The avalanche method involves paying off debt, which generally improves your credit score over time by lowering your credit utilization ratio. Unlike debt settlement, you’re paying balances in full — never missing or reducing payments.

Ready to Build Your Debt-Free Plan?

Use our free debt avalanche calculator — enter your debts, see your payoff date, and download your complete month-by-month PDF plan. No email, no signup.

✓ 100% free · ✓ No signup · ✓ Download PDF plan · ✓ 4,200+ users helped